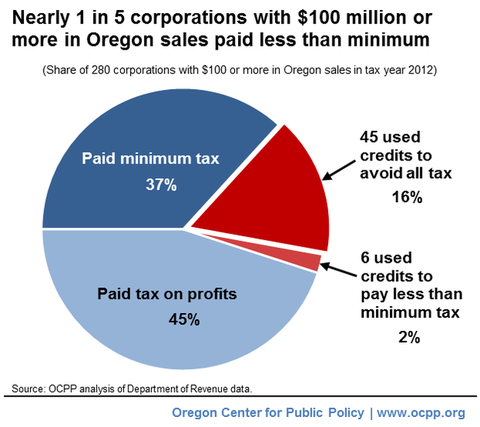

Corporation Tells Truth About Tax Subsidy

Published on Oregon Center for Public Policy by Chuck Sheketoff How refreshing it is to hear a...

Read More

Published on Oregon Center for Public Policy by Chuck Sheketoff How refreshing it is to hear a...

Read More

Published March 30, 2015 by Oregon Center for Public Policy Although Oregon has a minimum income...

Read More

by Chuck Sheketoff Oregon has one of the nation’s highest use of the Supplemental Nutrition...

Read More

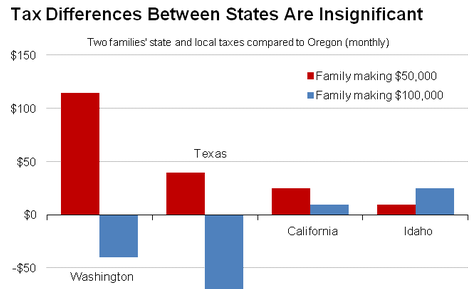

Published by Oregon Center for Public Policy Every state tax system in the country makes income...

Read More

Published October 7, 2014 by Oregon Center for Public Policy By Chuck Sheketoff Say that you’re...

Read More

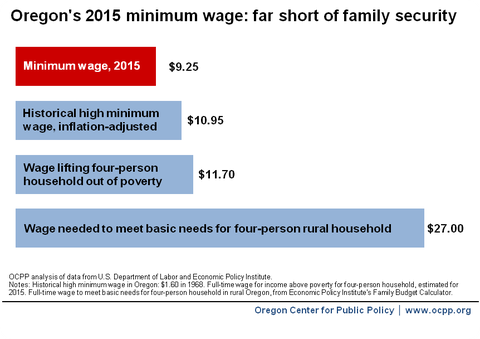

By the Oregon Center for Public Policy Oregon’s minimum wage will edge up 15 cents per hour next...

Read More

Published on August 20, 2014 by Oregon Center for Public Policy by Chuck Sheketoff Oregon has the...

Read Moreby Chuck Sheketoff Often I am asked, “What can we do to address income inequality?” There are a number of good ideas for confronting income inequality, which now stands at historic highs. In my view the first thing to do is to...

Read More

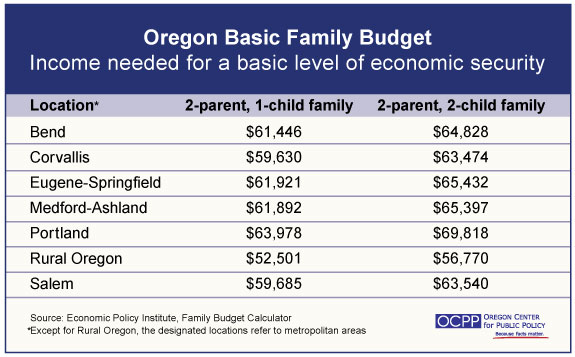

Published by Oregon Center for Public Policy How much income do families across Oregon need to get...

Read MoreState corporate income tax avoidance spans the nation

Read MoreThis one-page fact sheet (PDF) provides a long-term view of changes in income going to Oregon’s top 1 percent, compared to the 99 percent

Read MoreLow-income Oregonians are expected to make up the bulk of the state’s population who still won’t have health insurance –

Read More