All ye who are disillusioned and angry at our politicians’ and bureaucrats’ craven licking of Jordan Cove’s boots, take heart; don’t work yourselves into any more lathers over a process that never intended to turn down even the nastiest industrial promotion imaginable. Neither should you have been surprised that those politicians who got your vote by promising to work for you have produced nothing but grief. In Coos Bay, that’s been standard procedure for forty years; and we must deal with that, but not by running ourselves ragged by endlessly filing objections that are not read, and speaking at public meetings where nobody listens. Let’s face it: the deck was always stacked.

But to make up for this dour assessment, I am 99.8% convinced that in the end, Jordan Cove will simply melt away like so many sensational prospects before it. In reaching that conclusion I have considered the global LNG market that Jordan Cove’s parent, Veresen, has been so eager to cash in on, and also what Veresen itself is saying about its prospects. But before I get into that, I call on you to fill yourselves with a steely determination to finally put a stop to forty years of counterproductive nonsense like Jordan Cove. When they bow out, we must take advantage of the inevitable public hangover in order to take serious political action. Enough is enough; the only achievement of the ecodevo fanatics has been our impoverishment.

“Very long-term contracts”

To study what Veresen is really saying about its future we need to turn to a telephone conference call of November 8, conducted by the company’s CEO Don Althoff and some of his acolytes including Betsy Spomer, the latest “CEO” of Jordan Cove, who makes about half of what’s been offered to the next “CEO” of the Oregon Intestinal Port of Coos Bay. I thank Maryann for the link.

To study what Veresen is really saying about its future we need to turn to a telephone conference call of November 8, conducted by the company’s CEO Don Althoff and some of his acolytes including Betsy Spomer, the latest “CEO” of Jordan Cove, who makes about half of what’s been offered to the next “CEO” of the Oregon Intestinal Port of Coos Bay. I thank Maryann for the link.

Conveniently for us, the conference call came with a transcript. On page two, after the usual boilerplate warnings that whatever the company officials said was “subject to risk and uncertainty” or, less diplomatically, to be taken with a grain of salt, Althoff boasted that Veresen is doing well because “all of our cash flows today are supported by very long-term contracts.”

That’s proper and praiseworthy, except for two things. One is that Veresen’s stock has done surprisingly poorly, since after reaching the $18 to $19 level earlier this year it has dropped to between $10 and $11. And while it’s true that the dramatic drop in oil and gas prices has affected a lot of energy stocks, including big ones like Shell and Chevron, Veresen’s stock never even got a lift from the always breathlessly announced progress in Jordan Cove’s permitting process this fall. Although great wisdom is not always found in the stock market, in this case there may be some.

But the other, bigger problem is that Veresen doesn’t have the money to build Jordan Cove. So to get it built, the company will need to attract investors by proving to them that most of the terminal’s capacity has been sold on more of those “very long-term contracts.” The best contracts would be 20 years long, for either the purchase of JC’s LNG or its liquefaction capacity. The latter would apply if JC, instead of handling the entire process of buying gas and selling LNG after liquefying and shipping it, simply sold its liquefaction services to other LNG traders. This is done by so-called “tolling agreements”, where LNG traders pay to reserve a certain volume of liquefaction capacity, whether they use it or not. And this has been described by JC’s yellow-bellied boosters as the company’s magic key to financial heaven.

The trouble is, Veresen has been promising for three years that contracts of one kind or another would shortly be in the bag. Last year we were even told they now had signed “Heads of Agreement”. If you look up the definition of those, you will find that they are friendly statements of interest, but in no way binding obligations. Then last November we learned that Althoff was in Japan, “negotiating” for contracts. There was no second report telling us that he came back empty-handed, but that was acknowledged when FERC happened to ask about the contracts. To all such queries by FERC, Veresen or Jordan Cove has invariably promised they’d have them by the next quarter or next year. And despite all those delays, during the recent telephone conference Althoff announced that “Jordan Cove has gained widespread credibility in the market . . . Our negotiations with potential customers are advancing and we expect as we expected and we will extend through the end of 2015 and possibly into early 2016.” As near as I can tell from his tortured grammar, that means he will have contracts at the beginning of next year, not long from now. Holding our breath seems inadvisable.

What long-term view?

Althoff’s most recent promise of contracts will expire one year after he dismissed rumors about Jordan Cove’s shrinking prospects: “I get asked a lot nowadays if the low crude (oil) prices will have an impact on our project. I don’t believe it will. I believe our buyers take a long-term view of the marketplace,” he declared last January. But “a long-term view” may well be a euphemism for his prospective customers’ reluctance to sign on the dotted line. They may figure: What’s the rush? And Althoff’s claim that falling oil prices are irrelevant to Jordan Cove’s prospects suggests that he is either ignorant or trying to pull the wool over people’s eyes. Particularly in Japan and Korea, LNG import prices have long been tied to the price of oil. That’s because some power plants over there are equipped to burn either fuel, whichever happens to be cheaper. Pulling the wool over our eyes looks like a distinct possibility.

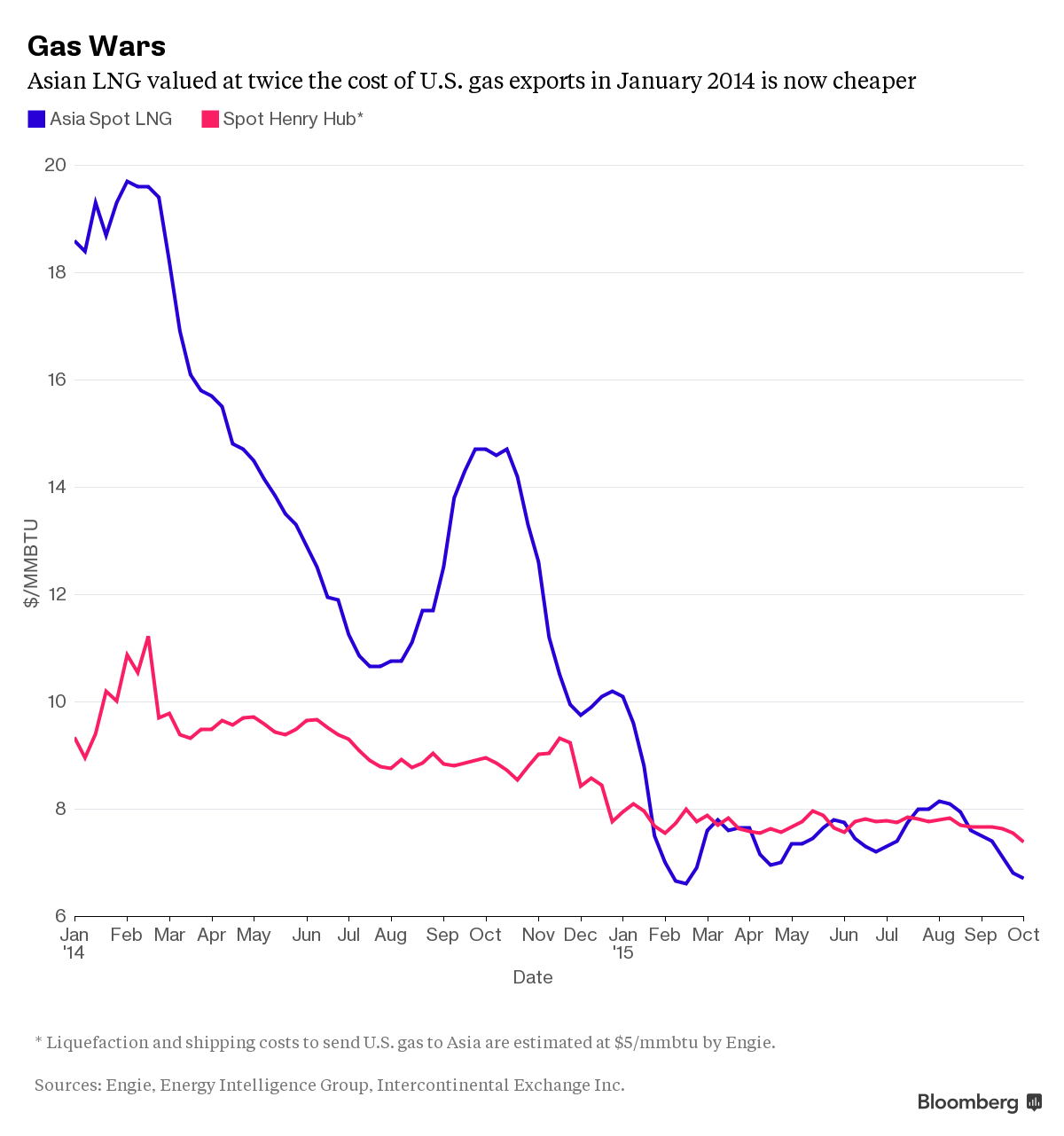

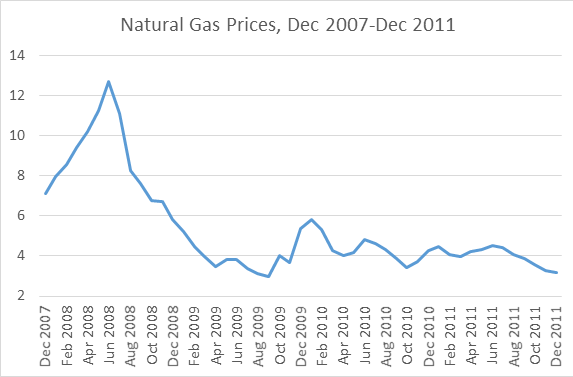

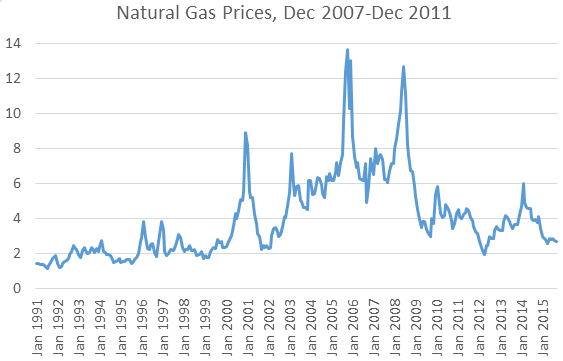

But while the price of oil has long been a factor affecting LNG prices in Asia, it is not the only one. To make money, international traders seek big price differences. Back in 2005 – 2007, natural gas prices in the US had risen to $12; and that was the foundation for Veresen’s proposal for an LNG import terminal. But it was a foundation built on shifting sand, as the old hymn puts it. For then the fracking boom made domestic prices crash back to $4, while LNG prices in Japan rose to $18 per MMBtu in 2012. Again responding to a big price difference, this time in reverse, Ve resen decided to change its now unviable LNG proposal from import to export. But the cause of those extremely high prices in Japan had been the Japanese government’s response to the meltdown of the Fukushima nuclear plant, caused by the earthquake/tsunami of the previous year. In what could be described as an over-reaction, all other Japanese nuclear power plants were taken off the grid too, with the shortage to be made up by burning LNG and other fuels. Suddenly LNG, which had accounted for 29 percent of the country’s energy mix, had to supply 46 percent of it. For sellers, it was great while it lasted.

resen decided to change its now unviable LNG proposal from import to export. But the cause of those extremely high prices in Japan had been the Japanese government’s response to the meltdown of the Fukushima nuclear plant, caused by the earthquake/tsunami of the previous year. In what could be described as an over-reaction, all other Japanese nuclear power plants were taken off the grid too, with the shortage to be made up by burning LNG and other fuels. Suddenly LNG, which had accounted for 29 percent of the country’s energy mix, had to supply 46 percent of it. For sellers, it was great while it lasted.

But recently the global LNG supply situation has eased, with many trade sources expecting years of oversupply due to new export facilities in the U.S., Australia, Indonesia and elsewhere. That, plus the fact that after careful investigations Japan’s nuclear plants are gradually being restarted, has pretty much destroyed any eagerness on the part of the Japanese to sign LNG supply contracts. More and more LNG is being sold at spot prices, which are now lower than contract prices – another novel development. Spot prices used to be higher than contract prices. Now that they’re lower, the supply of LNG is growing and sellers are eager to deal, the incentives to sign long-term contracts have almost vanished.

Flip-flopping away

If you consider all this recent history, it’s hard not to put a comical spin on it. While world markets were doing a fast flip-flop, our LNG promoters were doing their own fast flip-flop. But that may be all they ever do, considering Althoff’s lack of success with Asian buyers.

Still Althoff sounds as if he’s going full speed ahead and damn the torpedoes, since this April he bragged to Canada’s Financial Post about Jordan Cove: “I have got a $5 billion market cap and I am looking at a $7 billion capital project. I am going to spend a lot of money to get this project and its high-risk dollars.” As for those long-expected contracts, he hoped to have those “by the secon d quarter.” We’re now approaching the end of the year without contracts, and instead of $5 billion Veresen’s market valuation has gone down to $3.1 million, a 38% drop. Some potential investors may reckon that a $3.1 billion company that plunges $7 billion into a fluctuating market could be like a 100 pound swimmer who jumps in while attached to a 200-pound weight. So they will want guarantees in the form of signed contracts, an increasingly unlikely outcome. Althoff and many like him predict that the LNG market will balance by 2020-21. But that’s coming from people who had no idea that the most recent market flip-flops were at hand, and historically it’s been more common for commodity market ups and downs to last many more years. Moreover, LNG technology is changing. It’s conceivable that a few years from now, land-based terminals may be replaced by floating ones.

d quarter.” We’re now approaching the end of the year without contracts, and instead of $5 billion Veresen’s market valuation has gone down to $3.1 million, a 38% drop. Some potential investors may reckon that a $3.1 billion company that plunges $7 billion into a fluctuating market could be like a 100 pound swimmer who jumps in while attached to a 200-pound weight. So they will want guarantees in the form of signed contracts, an increasingly unlikely outcome. Althoff and many like him predict that the LNG market will balance by 2020-21. But that’s coming from people who had no idea that the most recent market flip-flops were at hand, and historically it’s been more common for commodity market ups and downs to last many more years. Moreover, LNG technology is changing. It’s conceivable that a few years from now, land-based terminals may be replaced by floating ones.

But Althoff says: “. . . even with all the noise in the LNG market today I still believe Jordan Cove is one of the best LNG projects in the market and that we will be able to sanction the project in 2016.”

I have to think of some shopping experiences I’ve had. As a rule I hate shopping, but there were a few times when I ventured into a place that was going out of business. Being a bargain hunter, I would ask the proprietor how business was, so his negativism would enable me to snatch up a bargain. But I found out that a real salesman who is going down the tubes will maintain that everything is just wonderful until the very moment his creditors evict him and lock his door. After all, what would be the point of admitting that you’re in trouble, and you may not survive? That would only make things worse.

In a publicly traded company the same thinking is at work, but it’s worse. The shareholders would be outraged if the CEO so much as hinted that the overambitious plan he’d already spent hundreds of millions on is unachievable – especially if he was still carrying on, burning up their money.

{kind=link}

It is fools like wim that have destroyed any chance Coos County will be anything other than the joke it is. Nobody will say with facts what is wrong with LNG hell for that matter everthing that stupid, even by Oregon standards, area has objected to. *! $” that area. I glad my family got over over and cheated that county long ago of all the rescoures it possibly could